%20-%20Credit%20management%20software.webp?width=1200&height=628&name=Blog%203%20(Nov)%20-%20Credit%20management%20software.webp)

Many finance teams spend 30-40 hours each week chasing invoices manually. DSO has crept from 45-70 days. Cash that should fund payroll, supplier payments, and growth sits locked in customer accounts, and credit lines carry the load at 7% to 10% interest.

At this point the decision is already made. Manual credit management is not sustainable. The real question is which credit management software will actually reduce DSO and bad debt without a painful 3 to 6 month implementation or yet another platform that the team uses at 5% of its capacity.

This guide compares 7 credit management platforms based on what mid-market finance teams actually need: rapid implementation, relationship-preserving automation, complete visibility, and proven ROI.

It covers features, implementation realities, pricing indicators, and real user experiences so you can choose a solution that delivers total control with ease of use rather than enterprise complexity and robotic communication that feel impersonal.

What to look for in credit management software

Think of this section as a short buyer checklist. These six criteria separate platforms that deliver from those that disappoint, regardless of vendor.

1. Implementation speed and integration stability

Mid-market teams can’t afford 6 to 12 month projects to replace spreadsheets. Look for implementations that complete in days to a few weeks, plus proven two way API sync with accounting systems like QuickBooks, Sage, NetSuite, or Dynamics. Avoid tools with a history of unstable connectors that create reconciliation errors or break billing when updates roll out.

2. Automation that maintains relationships

Executives often say poor AR communication directly causes nonpayment. Automation that sends generic dunning letters from a vendor domain increases that risk. So, prioritize platforms where reminders go from the business email domain, use the existing signature, and can be tailored so messages feel hand written rather than robotic.

3. Complete visibility across the team

Spreadsheet based chasing creates constant “who contacted whom and when” confusion. Finance leaders need a central hub that stores all chase history, promise to pay notes, disputes, and call outcomes. This is essential once more than a few users are involved and avoids duplicate outreach that frustrates customers.

4. Multi channel reach, not just email

Some customers respond to email, some to SMS, others to calls or letters. Email only tools are not enough. Look for platforms that combine email, SMS, phone, and portal messaging to drive higher response and payment rates, especially in diverse customer bases and regions.

5. Proactive risk management, not just reactive chasing

Bad debt can run 5-10% of revenue without proper controls. Effective credit management software uses AI scoring, credit bureau data, and behavioral history, to categorize invoice risk before the 30 day mark where collection probability starts to drop sharply. High risk accounts should appear in a clear priority list for the AR team.

6. Payment facilitation, not just reminders

Reminding customers is only half the equation. If payment is still inconvenient, cash remains stuck. Prioritize platforms with customer portals, multiple payment methods, payment plans, and automatic matching of payments to invoices. Customers who want to pay should be able to do it within a few clicks.

Platforms that consistently meet these criteria tend to serve mid-market companies best. The ideal fit is enterprise grade automation without enterprise level complexity or 12 month implementations.

The 7 best credit management software compared

|

Software |

Best for |

Capterra user rating |

|

Chaser |

Mid-market teams that want relationship centric AR automation and fast time to value |

4.9 / 5 (45 reviews) (Capterra) |

|

Invoiced |

Growing companies with complex, high volume billing that need deep AR automation |

4.7 / 5 (148 reviews) (Capterra) |

|

Billtrust |

Larger mid-market and enterprise firms needing advanced AI credit decisioning |

4.7 / 5 (33 reviews) (Capterra) |

|

Versapay |

Mid-market companies on NetSuite or Dynamics that want collaborative AR and payments |

4.4 / 5 (28 reviews) (Capterra) |

|

Kolleno |

Fast growing EMEA based firms needing highly configurable workflows and credit risk |

5.0 / 5 (8 reviews) (Capterra) |

|

Upflow |

Startups and scale ups seeking simple AR automation and strong analytics |

4.5 / 5 (15 reviews) (Capterra) |

|

Quadient AR (YayPay) |

Mid-market and enterprises that want deep ERP integration and predictive analytics |

4.5 / 5 (33 reviews) (Capterra) |

Ratings from Capterra UK as of 2026.

1. Chaser

Best for: Mid-market finance teams who need complete visibility and control over AR without enterprise complexity. Ideal when you're frustrated by scattered AR data, inefficient collaboration among team members, and manual chasing taking up 15+ hours per week.

Chaser combines credit control, multi-channel chasing, AI driven risk prevention, flexible payment options, and a central receivables CRM to help businesses build a solid credit management process.

This way, credit managers gain total control over schedules, templates, and escalation rules while automation keeps the relationship friendly.

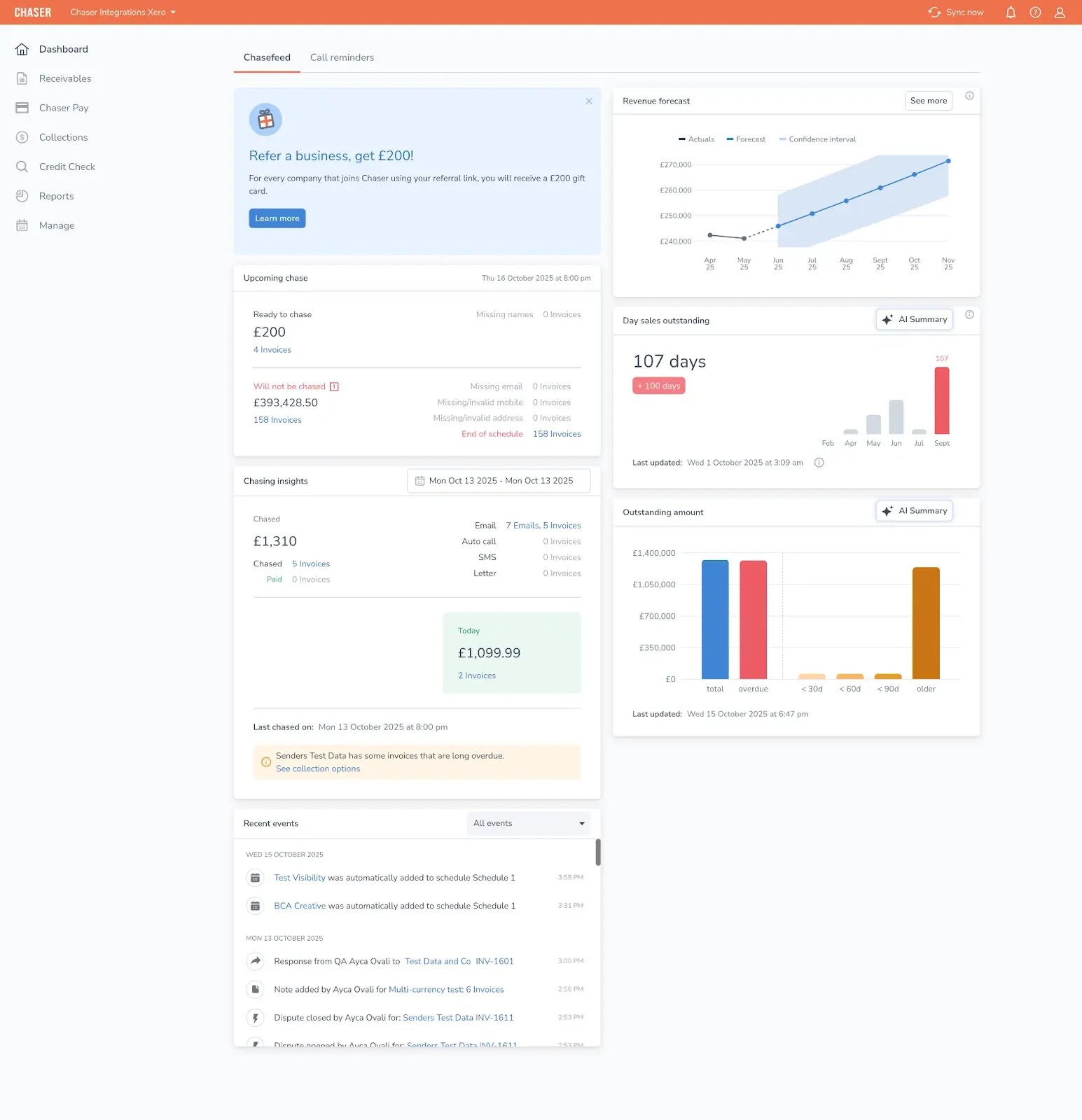

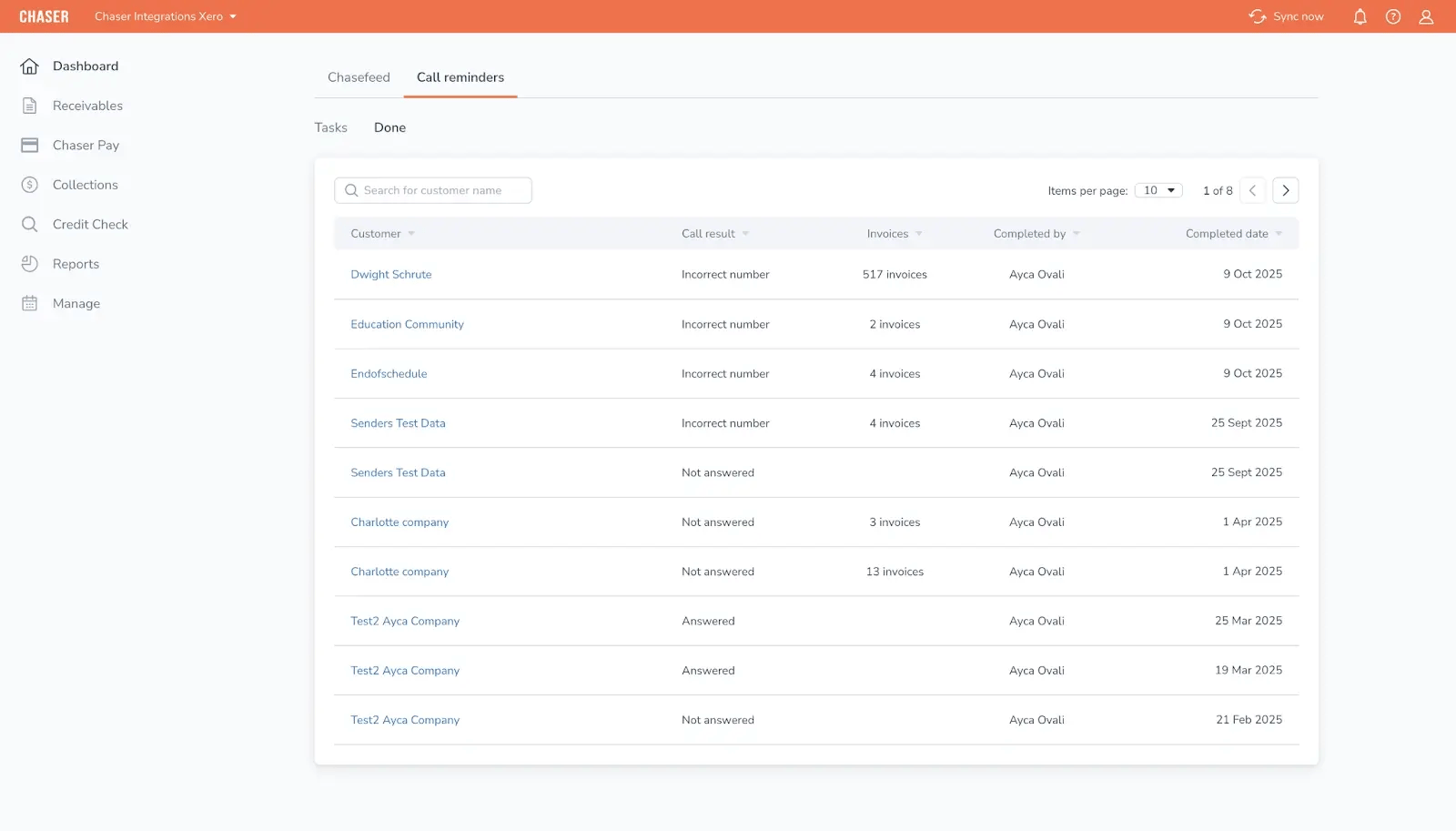

Maintain complete visibility and control across the entire AR function

One of the most frustrating parts of manual credit control is the lack of a shared picture. Different collectors maintain individual spreadsheets, email threads are scattered, and no one can see the full customer story.

Chaser solves this with a central Financial CRM for receivables. Every reminder, reply, phone note, promise to pay, and dispute is stored against the customer account. It is obvious who contacted whom, when, and with what outcome.

Two-way integration covers major accounting platforms including QuickBooks, Sage, Dynamics 365 Business Central, SAP, FinancialForce, and Epicor, with CSV and API options for others.

Mid-market finance teams who use Chaser see measurable impact within weeks. TaxAssist Accountants collected £20,000 in previously stuck invoices within 30 minutes and saved three weeks of annual staff time by eliminating awkward phone calls.

Prevent bad debt with AI powered risk prevention

Bad debt is where credit management becomes existential. For a $20 million revenue business, the difference between 2% and 6% bad debt is $800,000 a year.

Chaser’s Late Payment Predictor analyzes invoice due dates, values, and payment history to categorize each invoice as low, medium, or high risk with a simple percentage score. High risk invoices move to the front of the queue so collectors focus effort where it matters most.

The Payer Rating feature continuously reviews payment behavior and labels customers as good, average, or bad payers. That insight feeds both collections prioritization and credit decisions for new orders.

Built in credit checking and ongoing monitoring gives credit managers early warning when a customer’s risk profile deteriorates.

The overall effect is a shift from reactive debt chasing to proactive credit strategy, with data guiding decisions rather than internal politics.

Accelerate payment with flexible collection options and customer portal

Chasing is more effective if your payment collection process is easy. Chaser focuses heavily on reducing friction at that point.

The customer payment portal presents every outstanding invoice, previous payments, and downloadable statements in one place. That transparency removes common excuses such as “never saw the invoice” or “can’t find the right document.” Payment links appear directly in email and SMS reminders, and QR codes in letters can lead to the same portal, so customers move from reminder to payment in a single step.

Chaser Pay supports card payments, mobile wallets, and instant bank transfers in supported regions. For ERPs like QuickBooks and others, successful payments automatically mark invoices as paid, reducing reconciliation work.

With payment plans you can split large balances into installments without manual diary chasing. The platform automatically follows up on each installment according to the agreed schedule. Early payment discounts and late fees can also be configured to encourage timely payment and recover cost from persistent late payers.

All these make on time payment rates climb from roughly half of invoices to three quarters or more.

Chaser pros

- Replaces manual chasing with personalized automation that still feels human

- Strong focus on mid-market usability with fast implementation and minimal IT needs

- Flexible payment options that turn reminders into actual cash collection

- Integrated collections service for very late invoices without handing accounts to aggressive agencies

Chaser cons

- Advanced configuration options can take time to explore fully

- Best suited to B2B companies rather than very small micro businesses

Pricing

Chaser offers custom pricing tailored to your specific needs and invoice volume. The pricing page has more details.

A free trial is available to test the platform before committing. Typically, ROI is achieved within 6 to 18 months through DSO reduction and time savings.

What users say about Chaser

Chaser has a Capterra rating of 4.9/5 stars, with consistent praise for its ease of use, customer support, relationship preservation, reduced debtor days, and strong support.

One Capterra reviewer noted that Chaser “makes the chasing process simple with very little administration required” and reported a dramatic decrease in debtor days. Another described it as “sensibly priced, easy to use and extremely effective at streamlining the credit control process.”

Users also praise the ability to personalize templates so emails look as though they were written directly by the finance team, which supports relationship preservation.

Chaser gives mid-market finance teams complete visibility and control over credit management. With Chaser, you reduce bad debt and accelerate payment collections.

2. Invoiced

Best for: Mid-market to enterprise B2B teams that want broad AR automation in one platform, including invoicing, cash application,and recurring billing, plus strong accounting and ERP integrations. Best when you can absorb extensive implementation effort and premium pricing.

Invoiced, now part of Flywire, targets growing mid-market and enterprise companies with complex billing patterns such as recurring subscriptions, project based work, and multi entity setups. The platform focuses on full spectrum AR automation, including invoicing, subscription billing, collections, cash application, and customer payments.

Companies processing large volumes of invoices and payments often choose Invoiced for its breadth and for strong integrations with systems like QuickBooks, NetSuite, Sage Intacct, and Dynamics.

Key features

- Smart Collections with automated dunning across email, letters, and phone tasks

- AI based CashMatch for payment to invoice matching and virtual lockbox processing

- Subscription billing and recurring revenue management with dunning for failed payments

- Customer self service portal with multiple payment methods, autopay, and installments

- Rich invoicing capabilities for project based, usage based, and recurring billing

- Integrations with leading accounting and ERP systems plus open API for custom use

Invoiced pros

- Very strong for businesses with complex or extensive subscription billing needs

- Powerful automation across collections, billing, and cash application

- Self service portal reduces payment inquiries and supports multiple payment types

- Documented improvements in payment cycles and receivables within a few months of use

Invoiced cons

- Implementation for complex AR can be long and challenging, particularly for large portfolios

- Some history of integration issues, especially with QuickBooks Online, which created reconciliation errors when connectors changed

- Email based customer support and limited real time assistance can frustrate users who need fast resolutions

- Pricing is on the higher side for smaller firms

Invoiced pricing

Invoiced does not publish pricing on its website. Mid-market buyers should expect to engage with sales for a tailored quote based on invoice volume and integration complexity.

What users say about Invoiced

4.7 / 5 (148 reviews) (Capterra)

Recent reviews often praise forecasting accuracy and reduced reconciliation errors once the system is fully configured. Some users highlight significant time savings and improved visibility into AR. Others point to long onboarding processes and support that can be slow or difficult to reach, as well as pricing that’s more expensive compared to alternatives for similar functionality.

3. Billtrust

Best for: Mid-sized to large enterprises that need an end-to-end credit-to-cash suite with AI-driven credit decisioning, robust controls, and scalability across very high invoice volumes. A strong fit when you are standardizing credit, invoicing, collections, cash application, and payments, and you can handle the platform depth.

Billtrust is one of the most established vendors in the order to cash space, processing more than a trillion dollars in invoice value each year. The platform suits larger mid-market and enterprise organizations that want tight integration between credit, invoicing, payments, and cash application across multiple business units. Its AI powered credit decisioning and dynamic credit line management help organizations move beyond manual credit approval and review cycles.

Billtrust key features

- AI driven credit decisioning and auto approvals based on behavior and bureau data

- Dynamic AI credit lines that adjust limits as payment behavior changes

- Automated credit applications with trade reference collection and self service portals

- Integration with third party credit data providers for ongoing monitoring

- Centralized dashboards for credit reviews, customer blocking, and line adjustments

- Wide ERP integration coverage for SAP, Oracle, and other large enterprise systems

Billtrust pros

- Comprehensive end to end platform for credit, collections, invoicing, and cash application

- Long track record with large enterprises and high volume AR operations

- Strong AI capabilities for credit risk assessment and automated decisions

- Case studies show significant savings and improved cash flow for large clients

Billtrust cons

- Platform breadth can feel overwhelming, especially for teams without dedicated AR systems specialists

- Transitions between product generations have sometimes been difficult, with training gaps and lost features reported by users

- Dispute management capabilities have lagged behind some competitors, although recent features attempt to close this gap

- Pricing is opaque and often suited to larger budgets

Billtrust pricing

Billtrust does not publish standard prices. So expect to engage with them for quote based pricing.

What users say about Billtrust

4.7 / 5 (33 reviews) (Capterra)

Users frequently describe Billtrust as a great tool for streamlining invoicing and payments, highlighting time savings and a user-friendly interface once the learning curve is passed. Customer support is often praised for responsiveness. At the same time, some reviews call out challenging transitions to new platform versions and a feeling of feature overload that lengthens certain workflows compared to earlier versions.

4. Versapay

Best for: Mid-market companies that want embedded payments and strong ERP-connected automation, particularly in distribution, manufacturing, and services. A good choice when you care about customer self-service, collaboration on disputes, and cash application efficiency, assuming your reporting needs and ERP edge cases fit.

Versapay focuses on mid-market companies that want collaborative AR processes and embedded payments, particularly those using NetSuite, Microsoft Dynamics, or Sage Intacct.

The platform combines digital invoicing, collections automation, AI driven cash application, and a customer portal designed to promote real time issue resolution. It is especially attractive to organizations looking to reduce manual cash posting and connect AR closely with ERP processes.

Versapay key features

- Automated invoice delivery with click to pay links and embedded payment options

- Collections management with over 150 customizable reminder and escalation templates

- AI cash application achieving high straight through matching rates

- Integrated payment processing with next day funding and support for multiple payment types

- Credit management tools covering limits, history, risk analytics, and behavioral tracking

- Customer self service portal with statement access, dispute management, and promise to pay tracking

Versapay pros

- Strong native integrations with major ERPs, especially NetSuite and Microsoft Dynamics

- High levels of automation across cash application and collections that reduce manual workload

- Customer portal supports better communication, which reduces disputes and speeds up payment

- Documented ROI in the form of DSO reductions and manual processing time savings

Versapay cons

- Initial integration and onboarding can be more complex than expected, particularly for custom ERP environments

- Reporting, especially around DSO metrics, is an area some users feel could be richer and more intuitive

- Payment limits and complex multi invoice scenarios can present constraints for larger B2B transactions

- Occasional performance lags for large datasets, which can impact live customer calls

Versapay pricing

Versapay operates on a quote based pricing model with no figures published on its primary site.

What users say about Versapay

4.4 / 5 (28 reviews) (Capterra)

Recent reviewers describe Versapay as a major step forward from manual AR, citing fewer errors, better client communication, and reduced time spent on cash posting. Implementation is often described as worthwhile but not trivial, with training considered essential for teams new to digital AR tools. Users appreciate responsive support yet mention occasional system lag during heavy use.

5. Kolleno

Best for: Finance teams that want highly configurable collections workflows and an all-in-one AR stack with fast time to value, including risk and credit checks, portals, reconciliation, and analytics. Particularly compelling for scaling organizations that want sophisticated automation without extensive IT lift, as long as users can manage the configuration complexity.

.webp?width=1600&height=798&name=kolleno%20(1).webp)

Kolleno is an AI driven AR automation platform with strong presence in EMEA and a growing global footprint. It is designed by finance professionals and aims to give credit controllers deep control over workflows without extensive IT involvement. Mid-market and larger firms that need complex, branching workflows, advanced credit checks, and tight integration with ERPs such as NetSuite, SAP, and Dynamics often consider Kolleno.

Kolleno key features

- Dynamic collections workflows with multi branch logic and omnichannel communication

- Integrated credit and risk management with automated checks and real time alerts

- Customer payment portals with branded dashboards and multiple payment methods

- AI powered cash application and reconciliation across 150 plus currencies

- Integrations with a wide range of ERPs and CRMs, including legal practice tools

- Robust reporting and analytics with predictive insights and cash flow forecasting

Kolleno pros

- Highly flexible workflow engine that can be tuned precisely to business processes

- Rapid implementation timelines, often around 10-14 days, with minimal IT involvement

- Strong AI features that support prioritization, credit checks, and insight generation

- Customer support receives excellent feedback for responsiveness and ongoing guidance

Kolleno cons

- Power and depth of features introduce a learning curve, especially for users new to AR automation

- Some niche or legacy systems are not yet supported natively and may require custom work

- Mobile app experience could be richer for users who want to manage AR on the move

Kolleno pricing

Kolleno uses tiered per user pricing with different plans for small businesses, growing mid-market firms, and enterprises. A free trial is available.

What users say about Kolleno

5.0 / 5 (8 reviews) (Capterra)

Reviewers frequently mention strong time savings through automated reminders while still being able to add a personal touch to messages. Many highlight the clarity gained by having all payment information and history in one place. Some users note that advanced features can be confusing at first, but praise the customer success team for helping to configure workflows and explain capabilities.

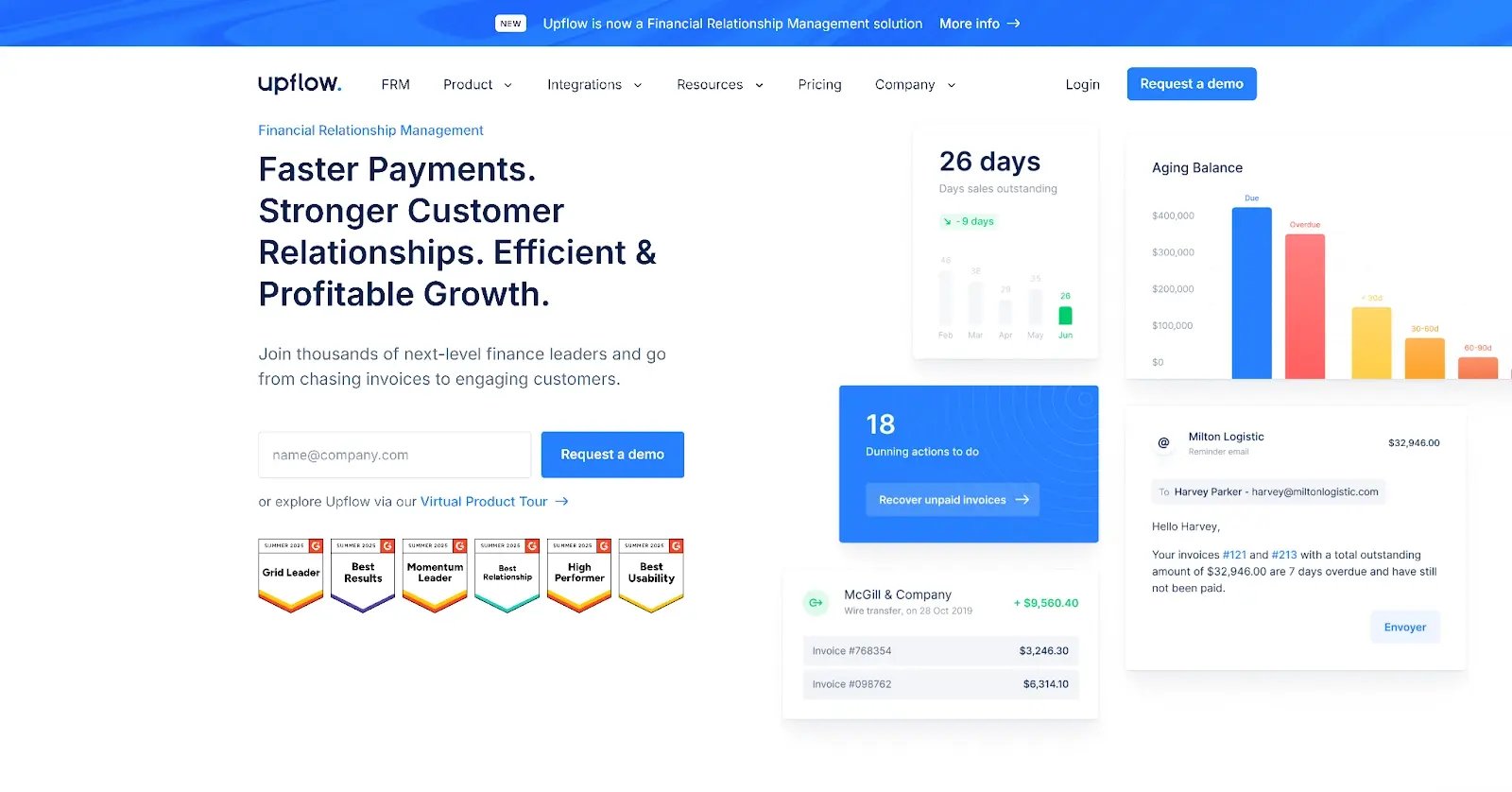

6. Upflow

Best for: B2B startups and scale-ups that prioritize relationship-preserving collections, fast onboarding, and cross-functional collaboration across finance, sales, and customer success. Ideal when you want workflow-driven dunning and modern payment UX with broad adoption, while accepting trade-offs in some workflow constraints.

Upflow positions itself as financial relationship management rather than just AR software. It is well suited to SaaS companies, tech startups, and scale ups with up to around 50 million in annual recurring revenue. The focus is on ease of use, clear dashboards, and collaboration across finance, sales, and customer success. Unlimited users and quick integration with tools like QuickBooks, Sage Intacct, NetSuite, Stripe Billing, and Chargebee make it attractive to growing teams.

Upflow key features

- Automated collection workflows with email, SMS, calls, letters, and tasks

- Branded customer payment portals with multiple payment options and autopay

- AI driven payment matching and reconciliation with high automation rates

- Real time dashboards for DSO, aging, and collection effectiveness

- Native integrations with accounting, billing, and CRM tools plus API

- Collaboration tools with unlimited user access and in app commenting

Upflow pros

- Very intuitive interface and quick onboarding, often live in a matter of minutes for simple setups

- Strong analytics and dashboards that replace manual spreadsheet reporting

- Unlimited users support cross functional collaboration without extra license cost

- Proven impact on DSO and late payment reduction for many SaaS and subscription businesses

Upflow cons

- Transparent pricing is limited and some users perceive the platform as expensive for its feature set

- Certain payment scenarios, such as immediate credit card charges or partial payments, have been cited as limitations

- Reliance on Upflow email domains can create spam perception unless custom domains are configured

- Workflow controls at individual invoice level are less granular than some competitors

Upflow pricing

Upflow offers a free discovery tier and paid plans for growth and scale, but does not list specific prices publicly.

What users say about Upflow

4.5 / 5 (15 reviews) (Capterra)

Users frequently praise the simplicity and effectiveness of the product, highlighting easier recovery through automatic reminders and action plans. Others describe it as a quality product that’s a bit expensive, and a minority report frustration when specific feature requests were not delivered over long periods. Overall, satisfaction scores remain strong, particularly around ease of use and support responsiveness.

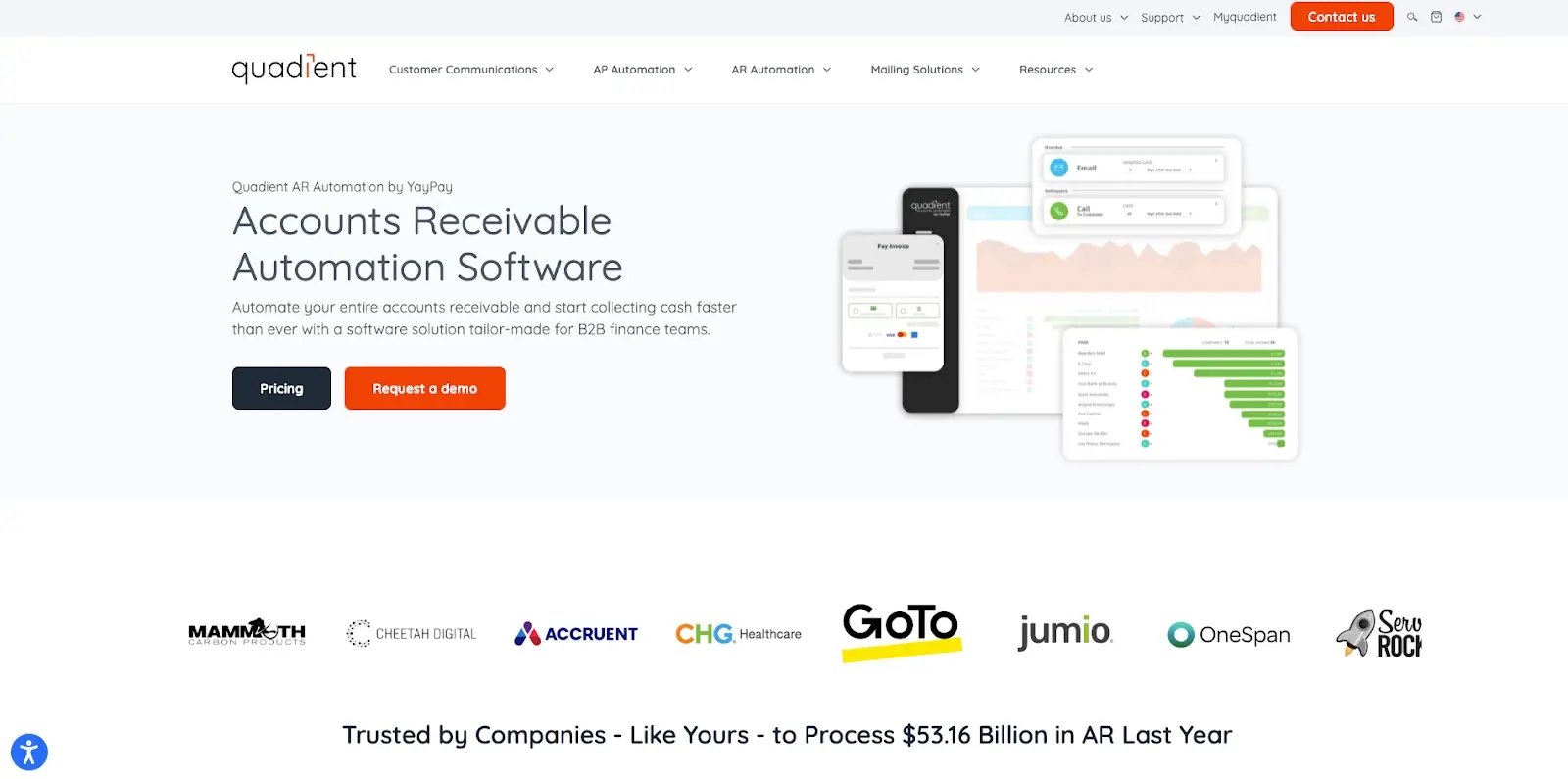

7. Quadient AR (powered by YayPay)

Best for: B2B finance teams moving from manual AR to automation who want an intuitive UI, strong credit risk tooling, and solid ERP connectivity. A good fit when ease of adoption and configurable collections matter most.

Quadient AR, formerly YayPay, is aimed at mid-market and enterprise organizations that want a unified credit to cash platform with advanced predictive analytics. Backed by a large parent company, the product offers strong credit management, collections automation, dispute handling, and cash application, along with extensive ERP integration. It is often chosen by firms that outgrew basic AR tools and want robust forecasting and credit risk capabilities.

Quadient AR key features

- Intelligent credit scoring with real time integration to bureaus such as Dun & Bradstreet

- Automated collections workflows driven by predictive analytics for payment behavior

- Multi channel invoice delivery, self service portals, and statement access

- Integrated payment processing with multi currency support and autopay

- AI driven cash application that reduces application time from days to hours

- Advanced reporting and dashboards with cash flow forecasting accuracy around 94%

Quadient AR pros

- Strong credit risk management capabilities that bring external and internal data together

- Powerful automation that can reduce DSO by up to 50% within a few months for some users

- Deep ERP and CRM integration with major systems like NetSuite, Sage, and Microsoft Dynamics

- Implementation and user training are often described as smooth, with helpful support teams

Quadient AR cons

- Reporting and search features could be more flexible, particularly for consolidated multi entity views

- Snapshot based sync in some setups means invoice updates are not always real time

- Some global localization aspects, such as date formats, are still oriented toward US practices

- Starting price sits at the higher end of the mid-market range

Quadient AR pricing

Quadient AR uses a custom quote model. Actual costs depend heavily on scale, integrations, and modules.

What users say about Quadient AR

4.5 / 5 (33 reviews) (Capterra)

Users often report substantial DSO reductions and a shift from reactive to proactive collections. One review described DSO being cut in half within 120 days, while others highlight easy to use interfaces and strong support that’s collaborative and responsive. The main criticism is that reporting and search could be more robust for complex multi subsidiary structures.

How to choose the right credit management software for your business

A comparison is only useful if it leads to a clear decision. This five step framework helps map current pain to the right platform.

Step 1. Identify the primary pain point

Start by deciding which problem is the most important.

- If you have a cash flow crisis and stretched credit lines, prioritize rapid implementation and proven DSO reduction.

- If you have manual process overload with 30-40 hours per week in Excel and emailing customers, choose a tool with multi channel automation and time savings.

- If you don’t want aggressive chasing to push your customers away, favor tools with personalization at scale and strong escalation controls.

- If you have payment friction and your customers are willing to pay but find it inconvenient, choose tools with payment portals and offer payment plans.

- If you want to cut down bad debt levels, look for strong AI risk prediction and credit monitoring.

Step 2. Match company size to platform complexity

- Under $5million revenue. Avoid complex enterprise platforms. Upflow or Chaser can be a better fit.

- $10-$100 million revenue. This is the sweet spot for Chaser, Versapay, Kolleno, Invoiced, Upflow and similar platforms.

- Above $100 million revenue. Enterprise offerings like Billtrust or Quadient AR may justify their complexity and cost. Chaser also has a plan (Complete) for businesses in this range.

Step 3. Assess implementation urgency

If relief is needed within 60 to 90 days, prioritize platforms known for fast onboarding and minimal IT involvement, such as Chaser. Where a dedicated project team and longer timeline exist, larger enterprise platforms become viable. As a guardrail, doubling vendor promised timelines often aligns more closely with real world experience.

Step 4. Align requirements with capabilities

Use a checklist drawn from the comparisons. Multi channel reminders, self service portals, dispute management, AI prioritization, ERP integrations, and budget tolerance should all appear. Eliminate any solution that fails on one or two must have items rather than hoping to work around gaps later.

Step 5. Test before committing

Run trials or pilots with real invoices. Involve the AR team that will work within the system to avoid buying software that is unusable. Test the integrations thoroughly using a realistic data set to avoid surprises after going live.

For most mid-market businesses, Chaser offers a strong balance of automation, relationship friendliness, implementation speed, and measurable DSO reduction at mid range pricing. However, if credit management is heavily intertwined with complex global ERP landscapes or requires very advanced bureau based modeling, platforms like Billtrust or Quadient AR may be more suitable.

5 common implementation mistakes to avoid" or "avoiding implementation pitfalls

New software solves problems only if implementation is handled properly. These pitfalls are common and avoidable.

1. Skipping data cleanup

Migrating disorganized spreadsheets and inconsistent customer records into a new platform creates bad reporting and misapplied chases. Clean customer names, contact details, and open invoice data before importing, and use CSV imports only after duplicates and errors are removed. This avoids reconciliation problems later.

2. Over automating without strategy

Turning on every automation rule at once can overwhelm customers with messages and damage relationships. Start with high risk segments and late payers, then expand as results become clear. Keep a human in the loop for sensitive accounts.

3. Weak team onboarding

If only one person understands the system, usage drops when that person is busy or leaves. Involve collectors and credit controllers in selection, provide hands on training, and roll out a core feature set first. This increases adoption and value.

4. Ignoring integration testing

Assuming integrations will work perfectly can lead to billing failures and double charging. Test each integration in a sandbox, run parallel operations for a short period, and agree rollback steps in advance.

5. No clear success metrics

Without a baseline, it is impossible to prove ROI. Capture DSO, bad debt percentage, and manual hours spent on AR before implementation. Review these monthly after going live to confirm progress toward targets.

Measuring credit management software ROI: What to track

To justify investment, finance leaders need measurable results. These metrics show whether the software actually works.

Days Sales Outstanding (DSO)

Track DSO monthly with value weighting so large invoices carry appropriate influence. Many industries sit around a median of 56 days, while top performers reach 30-45 days. Moving from 70 to 45 days at 30 million revenue can free roughly 1.6 million in working capital that can fund growth or reduce debt.

Productivity gains

Record how many hours per week staff spend on collections activities such as composing emails, building aging reports, and logging calls. A realistic target is at least a 50%reduction in manual effort, often more. For a mid sized company this can translate into over 4,500 hours saved each year, equivalent to more than two full time roles.

Bad debt reduction

Monitor written off invoices as a percentage of revenue. Effective credit management can move this from 5% toward the 1-2% range typical of well managed portfolios. For a 20 million revenue business, that shift can add about 600,000 to annual profit.

Secondary metrics

- On time payment rate. Aim to increase the share of invoices paid on or before terms from around 55% toward 75% or higher.

- Average days late. Measure how many days after the due date customers actually pay and track the trend downward.

- Dispute resolution time. Monitor how quickly disputes are logged and resolved. Shorter cycles mean faster cash and better relationships.

- Team satisfaction and retention. Less repetitive work reduces burnout and makes it easier to retain skilled collectors.

ROI timeline expectations

Quick productivity wins often appear within 30-60 days as automation replaces manual tasks. Material DSO improvements usually arrive over 3 to 6 months as workflows stabilize and customer behavior adjusts. Full ROI across bad debt, productivity, and financing cost reduction commonly emerges between 6 and 18 months, which aligns with independent research showing that the vast majority of AR automation projects deliver expected returns.

FAQ

%20-%20Uplow%20alternatives.webp?width=400&height=225&name=Blog%206%20(Oct)%20-%20Uplow%20alternatives.webp)

%20-%20Automate%20debt%20collection.webp?width=400&height=225&name=Blog%201%20(Oct)%20-%20Automate%20debt%20collection.webp)

%20-%20Automate%20debt%20collection%20(1)-1.webp?width=400&height=225&name=Blog%201%20(Oct)%20-%20Automate%20debt%20collection%20(1)-1.webp)